Inflation marches higher, hitting 8.5% compared to a year ago

REAL ECONOMY BLOG | April 12, 2022

Authored by RSM US LLP

Long ago and far away, it was once taught that inflation has long and variable lags. That still probably applies when setting policy, managing a portfolio or making longer-term investments as top-line inflation jumped by 1.2% in March to 8.5% on a year-ago basis, according to government data released Tuesday.

Inflation may soon find its peak, but that does not imply that significant relief is on the way in the near term.

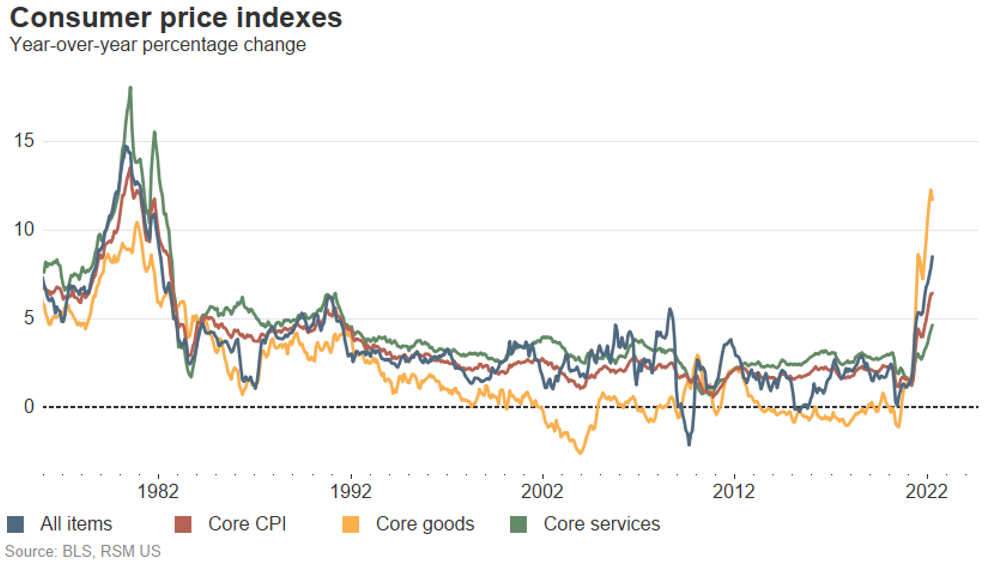

The increase in the core reading, which excludes food and gasoline, of 0.3% on the month and 6.5% on the year reaffirms that the price increases are broadening out beyond pandemic-induced inflation. Yes, inflation may soon find its peak, but that does not imply that significant relief is on the way in the near term.

Moreover, the cost of shelter increased by 0.4%, and the policy-sensitive owners’ equivalent rent advanced by 0.4% on the month. The cost of housing increased by 6.4% from a year ago, shelter by 5% and the owners’ equivalent rent of residences by 4.5%.

This element of the consumer price index report will prove persistent, sticky and most likely require policy attention to support an increase in housing supply. We are simply not building enough housing to meet demand driven by broad demographic changes in the economy, and that will need to change soon to address what we think will be a medium- to long-run challenge.

The March surge in inflation underscores the urgency at the Federal Reserve to push its policy rate higher, which is why more than 80% of investors now anticipate a 50 basis-point hike in the federal funds policy rate at the Fed’s May meeting.

In our estimation, that is likely to be followed by another 50 basis-point increase in June, which would bring the policy rate into a range between 1.25% and 1.50% by the middle of the year.

Declarations of inflation peaking under current conditions, when shocks from the global economy and geopolitical tensions could very well accelerate, should be taken as provisional at best.

Yet it is best that we do not confuse year-ago base effects with true relief for beleaguered households that find themselves with declining purchasing power that are quickly turning to draws on credit to meet basic needs.

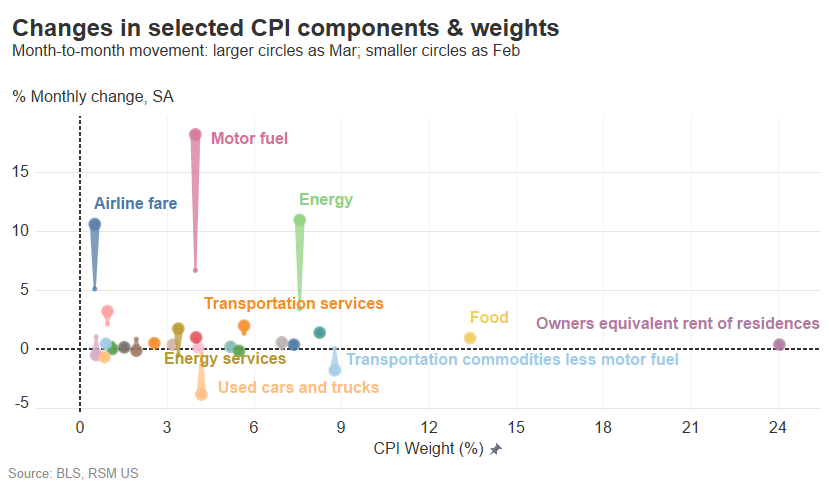

The only good thing that can be said about the March inflation data is that it just about perfectly captured the Putin price shock following the Feb. 24 invasion of Ukraine. The 18.3% increase in gasoline prices will ease in the April data, and that will bring down the top-line reading going forward.

The data

Excluding food prices, inflation increased by 1.3% on the month and rose by 8.5% from a year ago. Energy costs increased by 11% and have increased by 32% over the past year. Food costs jumped by 1% and have risen by 8.8% over the past 12 months. Excluding energy, inflation increased by 0.4% in March and rose by 6.8% over the past year.

Service-sector costs jumped by 0.7% and were up by 5.1% from a year ago. Fuel and utility prices jumped by 2% in March and increased by 12.5% compared to a year ago.

Food and beverage prices increased by 1% and have increased by 8.5% over the past year. A deeper dive into food prices indicates significant pricing pressure inside the food complex with a 2.8% monthly increase in rice, pasta and cornmeal; a 1.5% rise in food-at-home costs; a 2.1% increase in cereals; a 1% increase in meats, poultry and fish; and a 1.2% rise in dairy prices.

Food costs are likely to rise further this year as the conditions for a true global price shock within the food complex are present and will likely be clear to all this summer.

The cost of transportation increased by 3.9% in March and soared by 22.6% compared to a year ago. New vehicles increased by 0.2%, while the cost of used cars and trucks declined by 3.8% on the month.

Medical care increased by 0.5%, recreation costs by 0.2% and commodities by 2.1% while communication prices declined by 0.5% in March. Apparel prices increased by 0.6% on the month.

The takeaway

Price shocks continue to cascade through the U.S. economy. The risk of further oil and energy shocks—including the possibility that the European Union may cut off natural gas and oil imports from Russia—mean that policymakers, investors and firms should not prematurely declare a top on inflation costs. This will remain the case even as comparisons to the prices of a year ago make those numbers look slightly better going forward.

Sustained interest rate increases lie ahead, and given the long lags in inflation, we remain concerned that the 5.1% year-ago increase in service costs, which comprise much of the American economy, has not yet run its course. Most important, the increase in housing and shelter costs is going to be sustained and, in our estimation, will require policy attention over the medium term.

Let's Talk!

Call us at (800) 627-0636 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-04-12.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/inflation-marches-higher-hitting-8-5-compared-to-a-year-go/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Lewis, Hooper & Dick, LLC is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Lewis, Hooper & Dick, LLC can assist you, please call 1-800-627-0636.