How insurers can brace for inflation impact

ARTICLE | February 28, 2022

Authored by RSM US LLP

Property and casualty insurance carriers should be concerned as inflation continues to run hot throughout the global supply chain and is likely to increase the cost of claims for auto physical damage, property and catastrophe lines of business for years to come. The insurance ecosystem may be in for a rough ride this year because of the growing threat of social inflation affecting liability lines of business.

Parts and labor

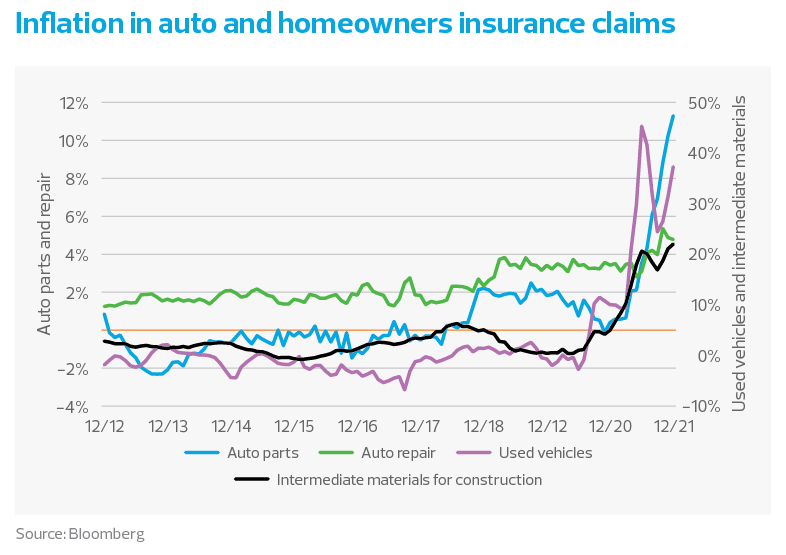

Inflation isn't a new risk for insurance carriers; over the last decade, there has been a steady increase in claim costs, particularly related to advances in automotive technology and the rise of extreme weather events. But there are more recent changes in technology, weather and supply chain disruptions to name a few that are putting more pressure on costs.

Traditional private passenger vehicles are transforming at a rapid pace into connected cars, equipped with technologies such as RADAR, LiDAR, advanced sensors, cameras and advanced driver assistance capabilities to meet the needs of consumers. A recent Fortune Business Insights study found that the connected car market in North America will exceed $60 billion in 2022. These new, tech-enabled automotive parts are more expensive to replace in the event of an insurance claim, and the repairs rely on highly skilled and costly labor.

Another factor is climate events, which are expected to continue increasing in frequency and severity, as we wrote about in our previous insurance sector quarterly outlook. Such climate events will continue to put pressure on carriers to manage the accumulation of risk implications within their business better.

Enter the pandemic and the exacerbated effects on claims inflation. Supply chain constraints have led to further increases in claim costs related to parts and intermediate materials, recent wage pressures and increased demand for used vehicles. Bottlenecks have also caused delays in the claim settlement process, resulting in higher costs for insurers as they provide their customers with rental vehicles and temporary housing.

Social inflation

The second side of the inflation coin that poses a growing threat to insurers is social inflation. This term is widely used by the insurance industry to describe rising claims costs over and above the economic inflation factors mentioned above, influenced by societal anti-corporate sentiment, trends and behaviors toward social responsibility. Understanding the numerous trends driving social inflation will help insurers proactively navigate the litigious environment the industry is facing.

Perhaps the most significant of these forces are public sentiment, tort reform and third-party litigation funding. Shifting attitudes about social injustices, inequalities and large corporations can factor into juror responses in claims cases, for instance. According to a 2020 study published by the American Transportation Research Institute, nuclear verdictsy, those with awards greater than $10 millions early doubled between 2010 and 2018 in insurance claim cases. Such ripple effects of social inflation can be hugely consequential for insurance pricing, actuarial work, underwriting, valuations and claims.

In addition to public sentiment, tort reform is driving social inflation. Tort reforms are designed to provide fair compensation and control costs. These types of reforms can limit how much a plaintiff can collect for noneconomic and punitive damages. Many state legislatures have struck down these types of caps on damages. Tort reform has also brought more challenges to statutes of limitations for lawsuits arising out of accident or injury claims. The statute of limitations is a legally established limitation period - ypically one to six years depending on the state - to pursue a legal claim. Extending the statute of limitations can potentially result in longer claims cycles, higher defense costs and higher jury awards.

Another contributing factor to social inflation is third-party litigation funding. Firms in this space provide funds to plaintiffs that could potentially result in large payouts in exchange for a percentage of any awards. These firms typically structure the investment as a prepaid forward contract instead of a loan to capitalize on gain tax benefits and are not restricted by a legal code of ethics. Third-party litigation funding might incentivize plaintiffs to pursue prolonged case settlements, hold out for larger recoveries or potentially increase unnecessary medical treatment options, for instance. Third-party litigation funding is a fast-growing multibillion-dollar global industry disrupting the insurance industry. According to a recent report by Swiss Re, third-party litigation funding totaled $17 billion in 2021, up 16% from 2020 despite pandemic-related delays and disruptions.

What can insurers do?

This inflationary environment is hitting the insurance industry hard in supply chain constraints, labor shortages and increasing litigation costs. Insurers are accelerating their business transformation plans centered around three primary themes to mitigate these risks: data, technology and talent.

Risk mitigation starts with data. Insurers use several methods to collect and analyze substantial amounts of information, such as process mining, statistical modeling and forecasting, and applying machine learning and algorithms. Data-driven insights help assess the capacity and performance of an insurer's network of suppliers and vendors, improve their ability to assess risk more accurately, optimize productivity and control costs.

Insurance is a heavy task- and transaction-based industry, and much of these tasks are still done manually. The mass exodus of skilled workers and unexpected retirements can pose workers compensation-related risks. To counter future supply chain disruptions and social inflation, insurers are accelerating their digital transformation strategies, including expansion of their vendor networks and partnerships, application of intelligent workflows and automation of underwriting tasks. Companies need to exploit technology to operate more efficiently and accurately assess risks.

Much like other industries are navigating the labor shortage, many insurers are paying higher wages, offering increased benefits and more work flexibility. Staying competitive in this environment requires sophisticated talent acquisition and retention strategies that go well beyond wage considerations. Companies need discipline and consistency in creating clearly defined and achievable career pathways through mentoring, upskilling and training to address skill and knowledge gaps.

The takeaway

The multifaceted effects of inflation on the insurance sector will continue to be an issue that companies need to navigate. Still, those that think strategically about how to use data and technology to boost efficiency and more holistically cultivate talent will likely be the most formidable competition.

Let's Talk!

Call us at (800) 627-0636 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by David Mamane, Marlene Dailey and originally appeared on Feb 28, 2022.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/economics/how-insurers-can-brace-for-inflation-impact.html

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Lewis, Hooper & Dick, LLC is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Lewis, Hooper & Dick, LLC can assist you, please call 1-800-627-0636.