FOMC policy decision: Fed hikes policy rate by 75 basis points

REAL ECONOMY BLOG | July 27, 2022

Authored by RSM US LLP

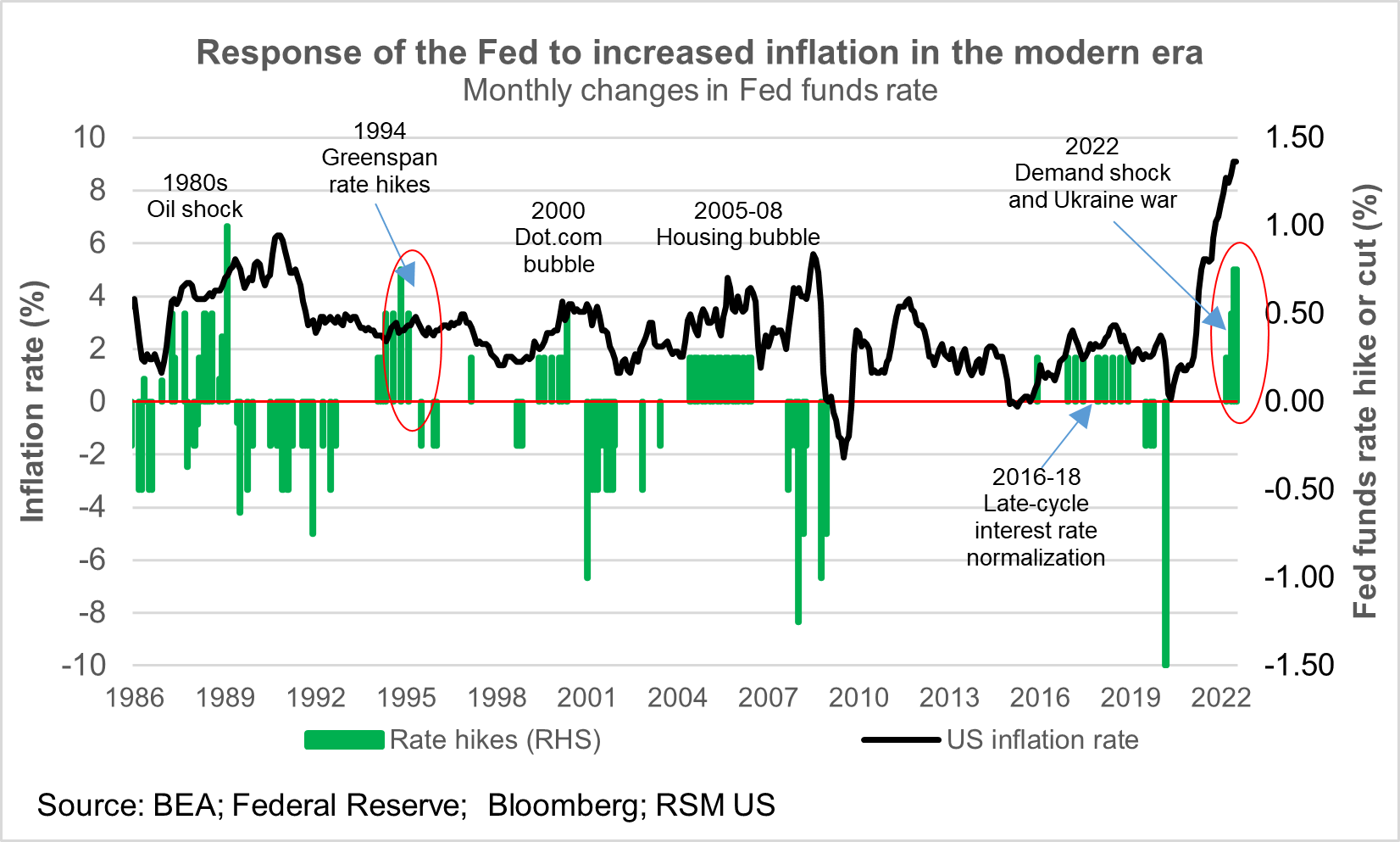

The Federal Reserve’s price stability campaign advanced at its Wednesday meeting via a hike in the federal funds policy rate by 75 basis points to a range between 2.25 and 2.5%. The central bank stuck to its pace of balance sheet reduction.

At this critical juncture, with the policy rate residing in neutral terrain, it is natural for the Fed to adjust its rhetoric as it considers next steps with respect to just how high it will choose to set the policy rate through the end of the year, given the obvious slowing in economic activity. The specter of rising unemployment will almost certainly be the result of the central bank’s attempt to restore price stability.

We do not anticipate that the Fed will consider any pause or pivot in policy until the federal funds rate reaches a range between 3.25 and 3.5% later this year, so any idea of rate cuts in the near term due to economic weakness will likely prove erroneous. More to the point, due to the broadening out—and likely persistence—of inflation, the Fed would be wise to lift the policy rate to 4% before considering any pause or pivot despite the market pricing in rate cuts by mid-2023.

We continue to make the case that market participants’ focus on the size of the hikes is misplaced. The far more important issues are just how far into restrictive terrain central bankers should lift the policy rate, and the point at which policymakers choose to take their feet off the monetary brakes. Their doing so would allow the economy space to further absorb the rate shock the Fed has imposed on the economy to restore price stability, which is the more important policy decision.

The outlook

All that being said, the 75-basis-point hike will likely be the last of the supersize rate hikes. We expect 50-basis-point hikes in the Fed’s September and November meetings, followed by a 25-basis-point hike to wrap up the year.

At the outset of his Wednesday press conference, Federal Reserve Chair Jerome Powell hinted that the Fed may choose to adjust the magnitude of rate hikes going forward, linking it to how the data evolves. While another oil or energy shock could conceivably cause the central bank to revisit large 75- or 100-basis-point hikes in the future, the onset of demand destruction in down-market households and inventory issues in the big box stores that service them would imply the probability that hikes that large are now in the rearview mirror.

Of course, given the visible slowing in the economy, this will all run the risk of ending the current business cycle and inducing a recession in 2023. In our estimation, only then will the Fed begin to observe a clear and convincing easing in inflation commensurate with moving back toward the 2% definition of price stability (the committee said in its Wednesday statement it is “strongly committed to returning to its 2% inflation objective”). Doing so over the next two to three years could conceivably lead to a pivot in policy and rate cuts. As of this writing, the market has priced in rate cuts in the second half of 2023.

Beyond the rate hikes, the only major change the Federal Reserve announced Wednesday was to the economic outlook, where the central bank said that “recent indicators of spending and production have softened.” In addition, it added food to energy prices in the pricing component to complement its economic outlook.

The takeaway

The Fed’s decision was an acknowledgement of the obvious slowing in the economy and will likely be interpreted as the Fed underscoring its commitment to restoring price stability despite that slowdown. There were no dissenting votes on this policy decision.

Let's Talk!

Call us at (800) 627-0636 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Joseph Brusuelas and originally appeared on 2022-07-27.

2022 RSM US LLP. All rights reserved.

https://realeconomy.rsmus.com/fomc-policy-decision-fed-hikes-policy-rate-by-75-basis-points/

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Lewis, Hooper & Dick, LLC is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Lewis, Hooper & Dick, LLC can assist you, please call 1-800-627-0636.