Estate planning Q&A: Qualified Personal Residence Trusts Explained

TAX ALERT | April 29, 2024

Authored by RSM US LLP

Many people want their loved ones to inherit their home after they are gone. However, leaving the value of your home in your estate can contribute to a high estate tax bill. Qualified Personal Residence Trusts (QPRT) can be a valuable tool to make a lifetime transfer of your home to your family, still enjoy the home during your life, and potentially reduce your estate taxes.

What is a QPRT?

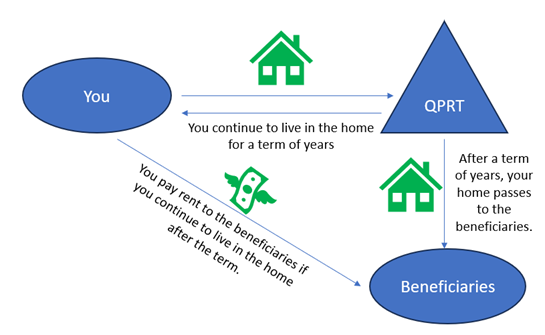

A QPRT is an irrevocable trust designed to reduce the amount of gift and estate taxes typically incurred when transferring a personal residence to beneficiaries. By transferring your home into a QPRT, you can continue living in it for a specified term while passing it on to your heirs at a reduced transfer tax cost. The essence of a QPRT lies in its ability to freeze (for estate tax purposes) the value of your home at the time of the trust's creation, potentially shielding any future appreciation from estate taxes.

What are the requirements for establishing a QPRT?

- Generally, the personal residence must be the sole asset of the trust.

- You decide on a fixed term (e.g., 5, 10, 20 years) during which you retain the right to live in the home. After this term, the residence passes to the beneficiaries designated in the trust. You may live in the home after the term, but you must pay rent to retain the estate tax advantages.

- Once established, the terms of the QPRT cannot be altered, and residence cannot be taken back

What are the benefits of setting up a QPRT?

- When you transfer your home into a QPRT, the value of the gift used for gift tax reporting purposes is calculated based on the current value of your home minus the value of your retained interest in living there for the term of the QPRT. Thus, the value of the gift is less than an outright gift.

- Any appreciation in your home’s value during and after the term occurs outside of your estate, potentially saving on future estate taxes.

- Payment of rent after the term is not considered a gift to the other QPRT beneficiaries.

- If necessary, the residence can be sold while it is owned by the QPRT.

What are the potential downsides of setting up a QPRT?

- If you die during the QPRT term, the entire home is included in your estate.

- Transfers made during life generally mean a carryover basis for your beneficiaries, leaving them with the burden of potential capital gains if they sell. If a QPRT is not utilized and the asset is included in your estate, there may be a step-up in basis, potentially avoiding capital gains.

- The payment of rent after the term can cause additional complications, such as determining the fair market rent, cash flow issues for the renter, or disagreements among family members.

- QPRTs may not be an efficient tool for multigenerational transfers because you cannot allocate your available generation-skipping tax exemption to the transfer until the end of the term, when values have likely increased.

- You must file a gift tax return and obtain a professional appraisal to establish the transferred interest's value for transfer tax purposes.

Is a QPRT right for you?

QPRTs offer a strategic way to pass a valuable asset to your loved ones. However, the decision to use a QPRT requires careful consideration of its benefits and limitations. In addition, it is important to properly administer QPRTs to avoid IRS scrutiny. By understanding the requirements, advantages, and potential downsides, you can make an informed decision about whether a QPRT is right for your estate planning needs. As always, consult with your RSM tax advisor to tailor a strategy that best suits your situation and goals.

Let's Talk!

Call us at (800) 627-0636 or fill out the form below and we'll contact you to discuss your specific situation.

This article was written by Scott Filmore, Amber Waldman and originally appeared on 2024-04-29.

2022 RSM US LLP. All rights reserved.

https://rsmus.com/insights/tax-alerts/2024/estate-planning-qa-qualified-personal-residence-trusts-explained.html

RSM US Alliance provides its members with access to resources of RSM US LLP. RSM US Alliance member firms are separate and independent businesses and legal entities that are responsible for their own acts and omissions, and each is separate and independent from RSM US LLP. RSM US LLP is the U.S. member firm of RSM International, a global network of independent audit, tax, and consulting firms. Members of RSM US Alliance have access to RSM International resources through RSM US LLP but are not member firms of RSM International. Visit rsmus.com/about us for more information regarding RSM US LLP and RSM International. The RSM logo is used under license by RSM US LLP. RSM US Alliance products and services are proprietary to RSM US LLP.

Lewis, Hooper & Dick, LLC is a proud member of the RSM US Alliance, a premier affiliation of independent accounting and consulting firms in the United States. RSM US Alliance provides our firm with access to resources of RSM US LLP, the leading provider of audit, tax and consulting services focused on the middle market. RSM US LLP is a licensed CPA firm and the U.S. member of RSM International, a global network of independent audit, tax and consulting firms with more than 43,000 people in over 120 countries.

Our membership in RSM US Alliance has elevated our capabilities in the marketplace, helping to differentiate our firm from the competition while allowing us to maintain our independence and entrepreneurial culture. We have access to a valuable peer network of like-sized firms as well as a broad range of tools, expertise and technical resources.

For more information on how Lewis, Hooper & Dick, LLC can assist you, please call 1-800-627-0636.